Dear Reader,

This post is a follow-up post from our earlier post on Public Transport Ticketing System posted last week. If you have not read that we urge you to click here and view it before continuing to read this blog.

This is our attempt to analyze the Automated Fare collection system by selecting a mix of countries including advanced economy countries, Asian economies, and nations spread across all the continents where fare collection systems are considered robust, diverse, and efficient.

Ambimat Electronics with its experience of over 4 decades of indigenously designing and manufacturing Payment products in India, wishes to draw the attention of our customers and readers of blog posts towards the Automated Fare collection system.

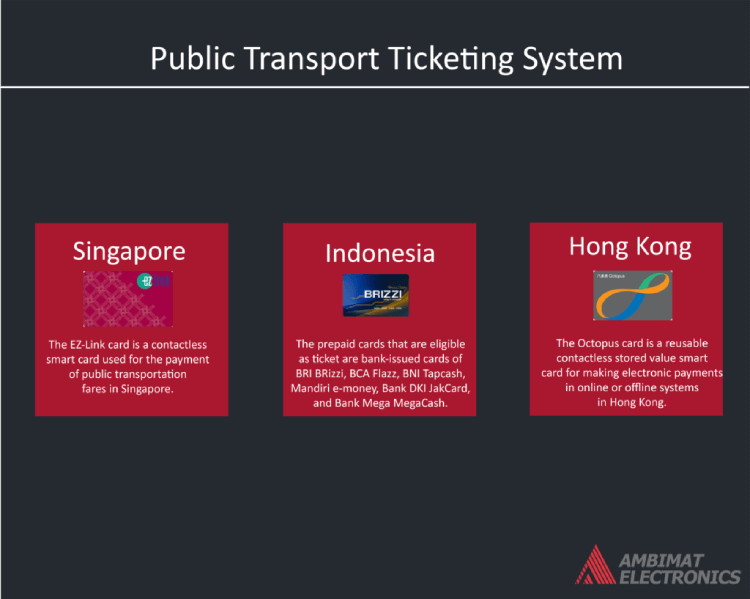

Singapore

Established in 2001, the first generation of the card was based on the Sony FeliCa smart card technology and was promoted as the means for speedier boarding times on the city-state’s Mass Rapid Transit (MRT), Light Rail Transit (LRT) and public bus services. It had a monopoly on public transportation fare payments in Singapore until September 2009, when the NETS FlashPay card, which had a monopoly over Electronic Road Pricing (ERP) toll payments, entered the market for transportation payments (and vice versa). EZ-Link cards are sold, distributed, and managed by EZ-Link Pte. Ltd., a subsidiary of Singapore’s Land Transport Authority.

In September 2009, the new CEPAS EZ-Link card replaced the original EZ-Link card, expanding the card’s usage to taxis, ERP gantries (with the dual-mode in-vehicle unit), car parks (which have been upgraded to accept CEPAS-compliant cards), convenience stores, supermarkets, and fast-food restaurants. Compared to NETS FlashPay, EZ-Link has lesser acceptance at retail shops.

The convenience and flexibility of the Singaporean ticketing system is an outstanding feature. The EZ-link card is the unified contactless stored-value card, introduced for public transport in 2002. The scheme successfully blends the major ticketing advances—it can be topped-up via multifunctional EZ-Link App, lets users earn and redeem reward points for all transactions made with the EZ-Link card, including non-transport services. In 2017 LTA piloted paying for bus and train rides with credit cards.

Indonesia

TransJakarta, the Bus Rapid Transit (BRT) system in Jakarta accepts e-tickets issued by several local banks. These e-tickets can be purchased at every TransJakarta shelter, banks (Mandiri, BCA, BRI, BNI, Bank DKI), and merchants such as minimarkets, supermarkets, and gas stations. The same e-ticket card can also be used in KA Commuter Jabodetabek (or more commonly known as Commuterline), the commuter rail system within Jakarta.

The Tap on Bus Validator is also available for ticketing services. The same is operational in TransJakarta, Trans Metro Bandung, Trans Jogja, etc.

Hong Kong

Hong Kong is actively applying modern technologies, and is among technological leaders. The city’s advanced ticketing system, Octopus chip card, is well known around the world as an example of innovative solutions. It is used by 99 percent of residents and can be used not only to pay for transport and non-transport services, but also for non-payment purposes, such as access control for office buildings.

Launched in September 1997 to collect fares for the territory’s mass transit system, the Octopus card system is the second contactless smart card system in the world, after the Korean Upass, and has since grown into a widely used payment system for all public transport in Hong Kong, leading to the development of Navigo card in Paris, Oyster Card in London, Opal Card in New South Wales, NETS FlashPay and EZ-Link in Singapore and many other similar systems around the world.

The Octopus card has also grown to be used for payment in many retail shops in Hong Kong, including most convenience stores, supermarkets, and fast food restaurants. Other common Octopus payment applications include parking meters, car parks, petrol stations, vending machines, fee payment at public libraries and swimming pools, and more. The cards are also commonly used for non-payment purposes, such as school attendance and access control for office buildings and housing estates.

About Ambimat Electronics:

With design experience of close to 4 decades of excellence, world-class talent, and innovative breakthroughs, Ambimat Electronics is a single-stop solution enabler to Leading PSUs, private sector companies, and start-ups to deliver design capabilities and develop manufacturing capabilities in various industries and markets. AmbiIoT design services have helped develop Smartwatches, Smart homes, Medicals, Robotics, Retail, Pubs and brewery, Security.

Ambimat Electronics has come a long way to become one of India’s leading IoT(Internet of things) product designers and manufacturers today. We present below some of our solutions that can be implemented and parameterized according to specific business needs. AmbiPay, AmbiPower, AmbiCon, AmbiSecure, AmbiSense, AmbiAutomation.

To know more about us or what Ambimat does, we invite you to follow us on LinkedIn or visit our website.

References:-

https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?TYPE=QUICK&PARAM1=2019&PARAM2=0